Over the past quarter-century, how have Emerging Markets and Developing Economies (EMDEs) fared, and what are their prospects for catching up with developed economies over the next 25 years?

Sergei Guriev, Dean of London Business School, introduced Ayhan Kose, Deputy Chief Economist at the World Bank Group, who discussed the January 2025 edition of the World Bank’s annual Global Economic Prospects report. Kose shared his insights on growth outlooks, poverty eradication by 2050, and the challenges that lie ahead in a conversation moderated by Lucrezia Reichlin, Professor of Economics at London Business School, alongside Rajesh Chandy, Tony and Maureen Wheeler Chair in Entrepreneurship, Co-Academic Director of the Wheeler Institute for Business and Development, and Professor of Marketing at London Business School.

At this pivotal juncture of the century, the Global Economic Prospects report explores the trajectory of EMDE growth over the next quarter-century. Hosted by the Wheeler Institute for Business and Development, Kose’s presentation offered valuable reflections on the near-term prospects in an increasingly uncertain economic environment, with a particular focus on low-income countries (LICs) and key policy priorities.

Near-term global economic prospects

Over the past three years, a surge in inflation led central banks to respond with sharp increases in interest rates, marking the first time such aggressive monetary tightening has occurred since the 1980s. Historically, such measures have typically resulted in slowdowns or even recessions. Yet, the global economy has displayed resilience, with growth projected at 2.7% in 2025. This stability is the result of contrasting economic trends—while certain sectors and regions have faced deceleration, others, notably the United States, have exceeded expectations.

For EMDEs, China’s growth is projected to slow, with expectations of a stabilisation at 4%. Excluding China and India, however, other EMDEs are witnessing an acceleration, driven by rising consumption and investment, facilitated by an expected decline in interest rates. Despite these positive trends, the pace of growth remains insufficient for EMDEs to significantly close the income gap with developed economies and substantially improve living standards.

Structural risks continue to pose challenges, including trade fragmentation, geopolitical tensions, shifts in policy in developed markets, and financial pressures on highly indebted nations facing elevated interest rates. The U.S. economy continues to outperform expectations, supported by a strong labour market and productivity gains. In contrast, China faces policy uncertainty, and global trade faces risks from prolonged policy instability, potentially leading to a protracted period of uncertainty with significant consequences for global economic integration.

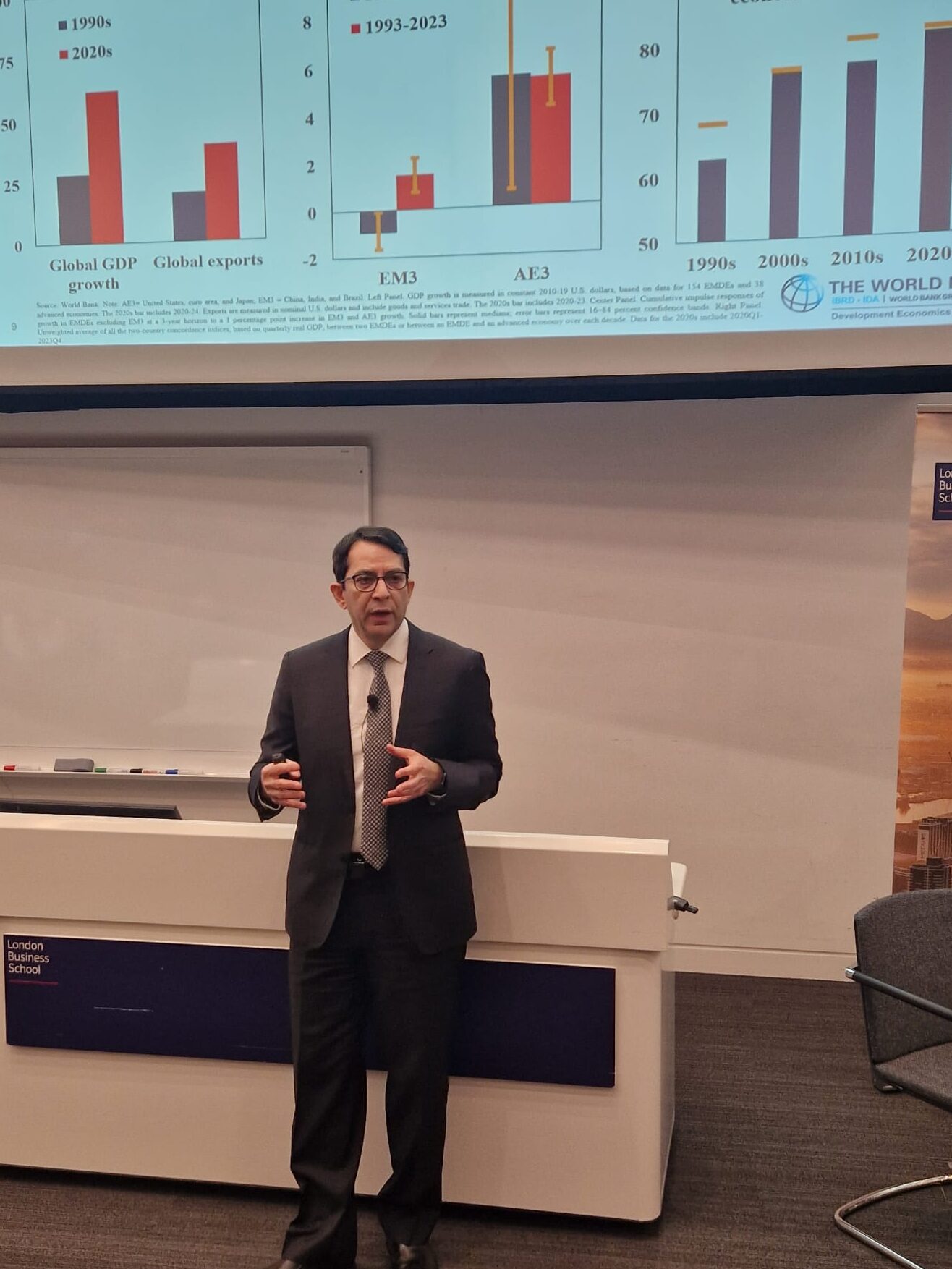

Emerging markets facing slower growth or reversal of early 2000s surge

At the beginning of the century, there was a broad consensus on the benefits of economic integration, trade, and openness. This translated into high growth rates during the early 2000s, with EMDEs experiencing growth of around 6% annually. This period of rapid expansion and integration resulted in increased production and consumption, reinforcing positive economic cycles in these regions.

However, after the first decade, growth slowed considerably, and projections for future growth diminished sharply. Investment and productivity declines contributed to a slowdown in trade, marking the end of a significant push for economic reforms. While EMDEs had previously been on a path of convergence with developed economies, this trend has now plateaued or reversed. Excluding China and India, many EMDEs are no longer catching up—they are, in fact, becoming poorer in relative terms. Trade, consumption, and foreign direct investment are all declining. In the 2000s, many EMDEs successfully reduced their debt levels, but in recent years, debt has increased due to government deficits rather than productive investment. Rising interest rates have increased fiscal challenges for these countries.

China, while expected to continue slowing in the coming years, retains considerable policy flexibility. Its investments in climate technologies, electric vehicles, and semiconductors offer some optimism for the future. However, the slowdown of China’s economy has broader consequences—its reduced growth no longer generates the same spillover benefits for other EMDEs. Consequently, other large emerging economies such as India, Brazil, and Indonesia will need to contribute more to sustain global growth.

Amidst debt, conflict and climate change, growth has been a challenge

Low-income countries (LICs) are defined by a per capita income of approximately $3 per day, placing them near extreme poverty levels. At the beginning of the century, there were 63 LICs. Rapid growth, domestic reforms, and a benign global environment enabled many former LICs to attain middle-income status in the 2000s. However, in recent years, progress has stagnated, and many LICs that did not transition to middle-income status have made little progress in reducing the poverty gap.

Sustained economic growth is key to enabling countries to graduate from LIC to EMDE status. Historically, this has required growth rates of at least 7%, maintained over extended periods (at least eight years). However, such growth accelerations are becoming increasingly rare in the current global economic environment. Based on current trends, fewer than one-quarter of LICs appear on track to make this transition by 2050.

LICs face multiple challenges, including high levels of debt distress, conflict-related instability, and adverse climate change effects that exacerbate food insecurity. Of the existing LICs, 17 are in active conflict, which diverts resources and attention from long-term economic planning. Though LICs account for only 1% of global GDP, they represent 9% of the world’s population, underscoring the urgency of finding sustainable development pathways.

Looking ahead at policy priorities

While the outlook for EMDEs and LICs is fraught with challenges, there are equally significant opportunities. No significant changes have been made to improve investment in climate, corruption controls or government spending, highlighting potential areas of growth. Additionally, many EMDEs possess abundant natural resources and attractive tourist destinations that could drive economic growth. LICs, in particular, have expanding working-age populations, which, if effectively leveraged, could attract global investment and spur development.

Investment decisions in EMDEs are increasingly influenced by human capital, capital growth potential, and, most critically, government policies that foster business-friendly environments. The role of independent and competent central banks in maintaining macroeconomic stability cannot be overstated. The so-called middle-income trap is not inevitable and countries such as India, Indonesia, and Bangladesh have demonstrated strong growth through strategic investments and sound policy execution.

Notable success stories include Nepal, which overcame internal conflict to achieve middle-income status in 2019, and Vietnam, which invested heavily in education and created business-friendly policies to enable sustained economic growth. However, in many LICs, ongoing conflicts must be resolved before long-term macroeconomic strategies can be effectively implemented.

In the face of climate challenges, LICs must focus on adaptation rather than mitigation. While their contribution to global greenhouse gas emissions is negligible, they face disproportionate consequences from climate change. Increased investment in infrastructure and climate adaptation is essential. Here, global cooperation is critical—governments and institutions like the World Bank must facilitate private sector investment by offering incentives such as risk protection mechanisms.

Finally, remittances—funds sent home by foreign workers—have become the largest capital inflow for many LICs, surpassing Foreign Direct Investment (FDI). While remittances can alleviate income disparities, their long-term economic impact requires further examination to determine if they provide the same growth stimulus as large-scale FDI projects.

There is no one-size-fits-all solution for economic growth. Countries that have successfully bridged the gap between LIC and EMDE status have implemented major policy changes. Reforms focused on digitalisation, climate adaptation, and improving the business environment will prove key in following decades and have potential to yield significant spillover benefits.

About the speaker

Ayhan Kose is the Deputy Chief Economist of the World Bank Group and Director of the Prospects Group, where he oversees global macroeconomic outlook, financial flows, and commodity markets. He leads the production of the Bank’s flagship reports, including Global Economic Prospects and Commodity Markets Outlook. Prior to the World Bank, Mr. Kose held key positions at the IMF, contributing to its analytical, policy, and operational work.

He has published extensively on international macroeconomics and finance in top academic journals and co-edited the book Falling Long-Term Growth Prospects, focusing on global growth drivers. His recent policy work addresses global inflation, debt challenges, and business cycles. Mr. Kose is also a Non-resident Senior Fellow at the Brookings Institution and has taught at prestigious institutions such as the University of Chicago’s Booth School of Business. He holds a Ph.D. in economics from the University of Iowa and a B.S. in industrial engineering from Bilkent University.

About the moderators

Lucrezia Reichlin is a Professor of economics at the London Business School, an external fellow at the Brussels based think-tank Bruegel, and Chair of the group of the National Schools of Economics and Statistics (GENES) in Paris. She is a macroeconomist and econometrician. She has pioneered methods for the economic analysis of large dimensional data and now-casting and co-founded the company now-casting limited in 2011. She was director general of research at the European Central Bank from 2005 to 2008. Professor Reichlin is a Fellow of the British Academy and the Econometric Society, an honorary international fellow of the American Economic Association, and a distinguished fellow of the CEPR.

Rajesh Chandy is Professor of Marketing and the Tony and Maureen Wheeler Chair in Entrepreneurship at London Business School, where he is also the Academic Director of the Wheeler Institute for Business and Development. Rajesh’s current research lies at the intersection of business and development. His recent projects have covered the impact of business skills among micro-entrepreneurs in South Africa, novel financing approaches in Ghana, property rights in slums in Egypt, innovation among farmers in India, highways and private education expenditures in India, and using big data for development outcomes.

About the author

Max Thomas is an MBA 2025 candidate at London Business School and an Outreach and Communications Intern at the Wheeler Institute for Business and Development. Prior to joining London Business School, he worked at McKinsey & Company as an associate in Brussels. Max is passionate about business as a force for good, and the impact education and healthcare systems have on human development.